Market Matters – The AI rally meets an inflationary reality

Summary

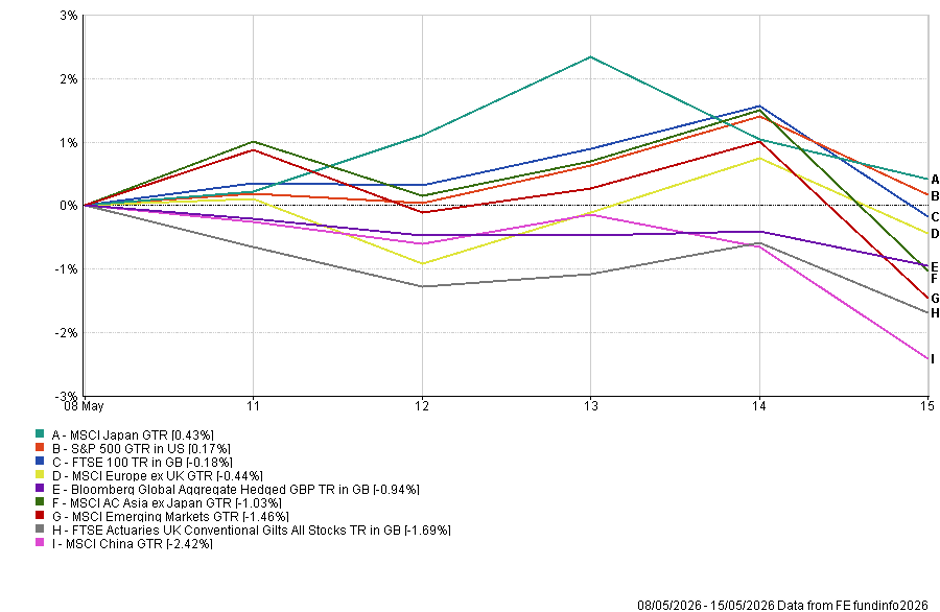

- Markets began the week positively but lost momentum as inflation and bond yields reasserted themselves. AI-related enthusiasm supported equities early in the week, particularly across semiconductors, memory, cloud infrastructure and wider data-centre supply chains. However, stronger US inflation data and a sharp sell-off in global bonds prompted profit-taking after a strong rally. Japan was the best major market, up around 0.4%, while the S&P 500 was broadly flat. China was weakest, down around 2.4%, and bonds were also under pressure, with global aggregate bonds down c.0.9% and UK gilts down c.1.7%.

- The AI investment case remains intact, but valuations are now being tested. The trade is no longer limited to the Magnificent Seven, with investors increasingly focused on the broader supply chain, including semiconductors, high-bandwidth memory, networking, storage, cloud infrastructure and power equipment. Korea and Taiwan remain especially important through Samsung, SK Hynix and TSMC. Real earnings and capital spending continue to support the theme, but after a powerful rally, the price investors are willing to pay is now more sensitive to inflation and higher discount rates.

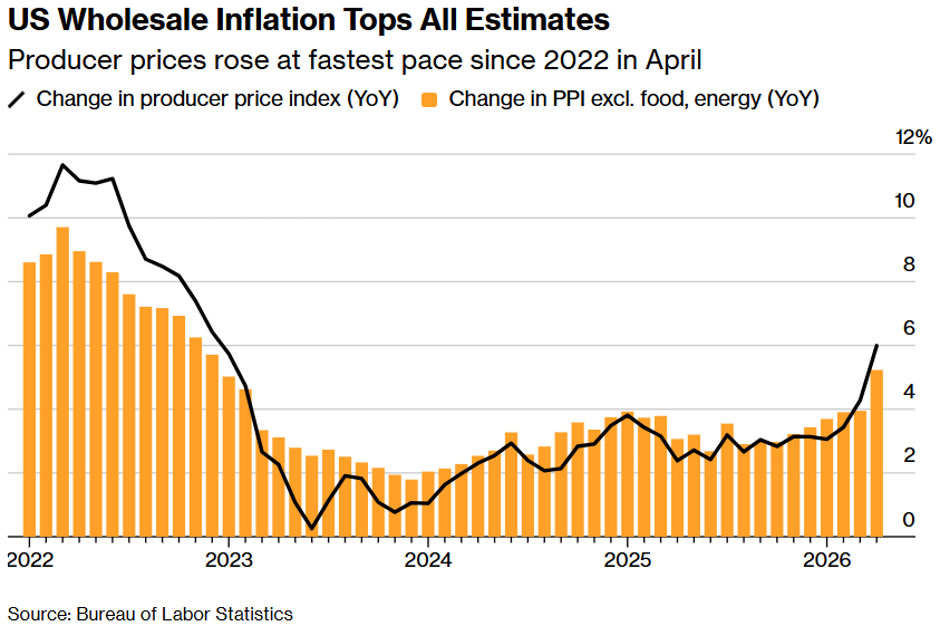

- US inflation was the key turning point, shifting the market narrative from growth optimism to policy constraint. Headline CPI rose to 3.8% year-on-year, while PPI was more concerning, with producer prices up 6.0% year-on-year, core PPI up 5.2%, and monthly PPI rising 1.4%. The issue is not just higher oil feeding into headline inflation, but the risk that energy, transport and freight costs start to pass through into food, goods, services and corporate margins. That makes the Iran/Hormuz shock inflationary first, with the growth drag likely to follow later.

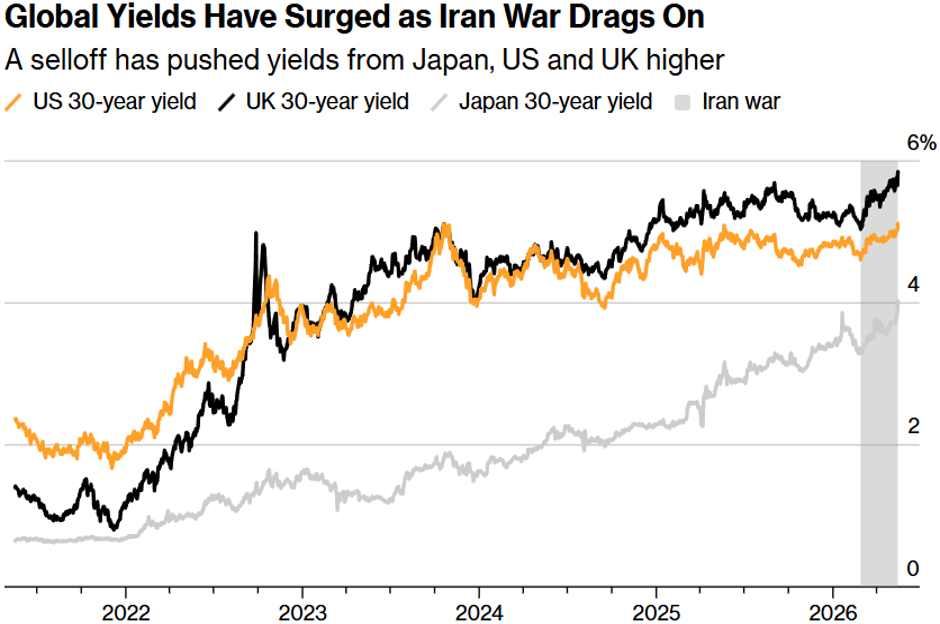

- Bond markets reacted badly, reinforcing the risk that duration is not a clean hedge in an inflation shock. Yields rose across the US, UK, Japan and Europe, with the long end of curves under particular pressure. US 10-year yields moved toward 4.6%, while UK gilts sold off sharply and long-dated gilt yields reached levels not seen for decades. If oil stays elevated and central banks are forced to think about tighter policy rather than cuts, longer-duration bonds remain vulnerable. This is especially relevant for the UK, where fiscal and political uncertainty added to global bond pressure.

In summary? The near-term outlook remains constructive but more fragile than a week ago. Earnings momentum, AI capex and resilient US growth still provide support, and investors remain willing to buy market dips. However, risks have clearly risen: the Fed has less room to support markets, Europe remains exposed to the energy shock, China remains weak, and the Strait of Hormuz remains unresolved with Brent above $109. NVIDIA’s results are the next key catalyst, as markets look for confirmation that AI infrastructure demand remains strong enough to offset the more difficult inflation and bond-market backdrop.

Full Overview

For the first time in several weeks, the Iran conflict was not the dominant day-to-day market headline, but it remained the unresolved macro risk sitting behind almost everything else. Markets began the week in a relatively confident mood, helped by ongoing enthusiasm around AI infrastructure, semiconductors and memory stocks. However, that optimism faded as the week progressed, amid stronger US inflation data, a sharp global bond sell-off, and renewed concern about second-round effects from higher oil prices, forcing investors to reassess how clean the outlook really is.

Market performance reflected that shift. Japan was the best major market, rising around 0.4%, while the S&P 500 was broadly flat after reaching fresh highs earlier in the week. The FTSE 100 slipped around 0.2%, Europe ex-UK around 0.4%, Asia ex-Japan around 1.0%, emerging markets around 1.5%, and China was the weakest major market, down around 2.4%. Bonds were also under pressure, with global aggregate bonds down around 0.9% and UK conventional gilts falling around 1.7%. The pattern was clear: risk assets had travelled a long way quickly, and the inflation data gave investors a reason to take some profits.

The AI story itself remains intact. The early part of the week continued the trend we have seen for much of the year: investors are no longer just buying the Magnificent Seven, but are increasingly looking at the wider AI supply chain. Semiconductors, high-bandwidth memory, storage, networking, photonics, cloud infrastructure and power equipment are all becoming central beneficiaries of the AI capex cycle. Korea has become particularly important because Samsung and SK Hynix sit at the heart of the memory bottleneck, while Taiwan remains critical (for now) through TSMC’s role in leading-edge chip production.

The important point is that real earnings and real capital spending are still supporting the AI trade. Hyperscalers continue to spend heavily, cloud revenues remain strong, and the demand for compute is flowing through into the companies that enable AI infrastructure. This is why equities have remained resilient despite oil prices, geopolitical risk, and a more difficult bond market. However, after a strong rally, the market became more sensitive to valuation and discount-rate risk. The AI thesis has not broken, but the price investors are willing to pay for it is now being tested by inflation and yields.

U.S. inflation pressures are building. The inflation data were the main turning point. US CPI was uncomfortable enough, with headline inflation rising 3.8% year-on-year and energy again a major driver. Core inflation also remained firm, reminding investors that the disinflation process is no longer smooth. The bigger concern came from PPI, where producer prices rose 6.0% year-on-year and core PPI increased 5.2%, both well above expectations. Monthly PPI rose 1.4%, with energy, transportation and warehousing costs particularly strong. Freight costs, trucking, fuel retail margins and broader services prices all suggested that the oil shock is beginning to bleed into the production pipeline.

That matters because the concern is no longer simply that higher oil lifts headline inflation for a month or two. The bigger risk is that higher energy and transport costs are gradually passed through to food, goods, services, and corporate margins. Once companies start passing on costs or protecting margins by raising prices, the shock becomes harder for central banks to ignore. This reinforces the idea that the Iran/Hormuz shock is inflation-first but growth-second: it raises prices immediately, then squeezes real incomes and demand with a lag.

The bond markets reacted accordingly. Yields rose sharply across the US, UK, Japan and Europe, with the long end of curves under particular pressure. US 10-year yields moved toward 4.6%, while long-dated Japanese yields reached historic levels, and UK gilt yields came under renewed pressure. This is exactly the regime we have been concerned about: duration does not behave like a clean hedge when the shock is inflationary rather than purely growth-driven. If oil stays elevated and central banks are forced to think about hikes rather than cuts, longer-duration bonds become vulnerable.

The Fed now has less room to be supportive. The US economy is still resilient, the labour market has not broken, and earnings remain strong. That gives policymakers little reason to look through inflation prematurely. Markets are now starting to price the possibility that the Fed may need to stay tighter for longer, or even tighten again, if inflation expectations and pipeline pressures continue to rise. The same issue is visible in Europe, where the ECB is increasingly likely to move toward a June hike unless the energy shock fades quickly. Europe’s growth backdrop remains weak, but the ECB is unlikely to ignore a renewed inflation impulse.

The UK had a particularly difficult week. The economy grew by a stronger-than-expected 0.6% in the first quarter, but that may prove to be the high point for the year. Higher energy prices, weaker consumer demand and tighter financial conditions are likely to weigh on growth from here. At the same time, political risk has risen after Labour’s heavy local election losses and Andy Burnham’s move toward a potential return to Parliament. The market concern is not simply personality politics; it is whether political pressure leads to a looser fiscal stance at a time when the gilt market is already sensitive to borrowing, inflation and credibility.

Gilts sold off sharply, with long-dated yields reaching levels not seen for decades. Some of that reflected the global bond sell-off, but UK-specific political and fiscal concerns clearly added to the move. Sterling also weakened. The lesson from the week is that the UK remains vulnerable to a difficult mix: stronger near-term GDP data but weaker forward momentum; higher inflationary pressures but limited room for the Bank of England to cut; and political uncertainty that could unsettle a bond market still scarred by 2022.

China and the US also remained in focus. Trump’s visit to Beijing did not deliver a clear breakthrough on Iran or Hormuz, but it also avoided a major flare-up over tariffs, Taiwan or technology restrictions. In the current environment, the absence of deterioration is itself mildly helpful. China has called for Hormuz to reopen, and both Washington and Beijing have an interest in lower energy prices, even if they remain on different sides of the broader geopolitical argument. Trump’s attention may now return more fully to the Middle East, where the stalemate is becoming increasingly costly for everyone involved.

Hormuz remains quiet(er), but not solved. Some tanker movements have improved, but flows are still far below normal, and shipowners remain cautious. Oil ended the week higher, with Brent back above $109. The longer the Strait remains disrupted, the greater the chance that the inflation shock becomes embedded through transport, supply chains and consumer expectations. Iran may believe time is on its side, but its own economy is also under pressure if oil exports remain restricted. The current position is increasingly unsustainable, which means either diplomacy must deliver soon or the risk of renewed escalation rises.

Europe remains the region most exposed to this energy shock. Growth is weak, the ECB is constrained, and higher energy prices feed quickly into inflation and industrial margins. If Hormuz reopened durably, European cyclicals could bounce sharply, but until then, the region remains vulnerable. Asia and emerging markets are more mixed. Korea and Taiwan remain AI winners, but broader EM and Asia are not immune to higher oil prices, stronger yields, and risk reduction. China’s weakness last week also reminds us that not all Asian exposure is benefiting equally from the AI hardware theme.

This week…

The key question is whether markets can find a fresh catalyst after such a strong run. NVIDIA’s results next week will be central to that. If the numbers confirm that AI infrastructure demand remains strong, and that hyperscaler capex is still flowing into chips, memory, networking and data-centre capacity, they could be enough to reignite the AI trade. However, expectations are already high, and with the broader US earnings season now largely behind us, there may be less room for disappointment.

That makes the summer more difficult to navigate. Markets still have support from earnings, AI capex and resilient US growth, but they also look more vulnerable to inflation surprises, higher bond yields and profit-taking after a powerful rally. Without a durable reopening of the Strait of Hormuz, oil is likely to remain a source of pressure on inflation, consumers and central banks. I don’t think this is the time to de-risk. I think there is enough momentum in the markets and plenty of investors willing to buy the dip, but it certainly feels less comfortable than a week ago. Let’s see if we can get some good news out of Nvidia and around the whole Iran conflict – now that the China summit is out of the way, I think that will be back at the top of Trump’s agenda.

Tom McGrath 17.05.2026

Edited by Ash Weston 17.05.2026

DOWNLOADS

There are currently no downloads associated with this article.