Market Insight – AI Takes a Breather

Summary

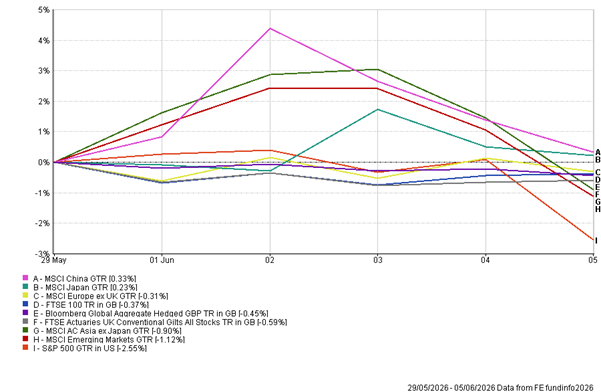

- Markets suffered a concentrated AI-led correction rather than a broad risk-off move. The S&P 500 fell 2.55% over the week, with the most acute weakness in AI-linked and semiconductor-heavy areas following Broadcom’s results. Regional markets appeared more resilient, but Asia and Europe had not fully reflected Friday’s late US sell-off, making the next open an important test.

- The AI investment case remains intact, but valuation discipline is returning. Broadcom did not undermine the structural AI infrastructure thesis; rather, it failed to meet a market priced for NVIDIA-style upside. The key issue is not whether AI demand is real, but whether some share prices had discounted too much good news too quickly.

- Strong US labour data reduced hopes of near-term Fed support. Non-farm payrolls rose by 172,000 in May, well ahead of expectations, with prior months revised higher and unemployment steady at 4.3%. This pushed yields higher and reinforced the risk that resilient growth, elevated oil and sticky inflation keep policy tighter for longer.

- Geopolitical risk remains a live inflation threat. The Middle East ceasefire remains fragile after fresh US-Iran exchanges and continued regional attacks. Brent near $93 and WTI above $90 suggest markets have moved from acute Hormuz panic to a more persistent duration-risk premium, with implications for fuel, transport, food and producer costs. The base case remains constructive, but the short-term narrative is being tested. This looks more like a valuation reset than a bubble bursting. A period of consolidation could be healthy if leadership broadens beyond crowded semiconductor names, but if weakness spreads into credit, defensives and broader earnings expectations, the signal will become more concerning

Full Overview

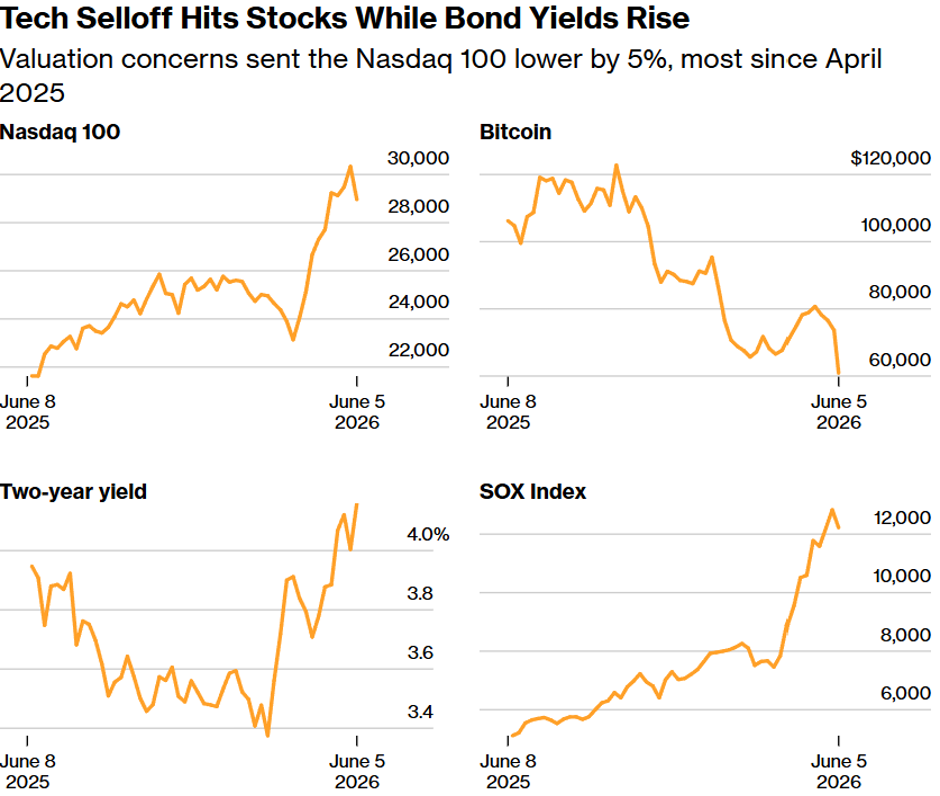

Markets finally had the wobble many had been expecting. After a powerful rally from the March lows, the AI and semiconductor trade came under pressure last week, with selling building after Broadcom’s mediocre results on Wednesday night and accelerating sharply into Friday’s US close. The S&P 500 fell 2.55% over the week, but the damage was much more severe in AI-linked and semiconductor-heavy areas. Elsewhere, the weekly regional numbers need some care. Japan and China edged higher, Europe ex-UK was only modestly lower and the FTSE 100 barely moved. On the surface, that suggests the sell-off was contained mainly within US growth and semiconductors. However, the sharpest part of Friday’s US decline came after Asia and Europe had already closed. Monday’s open will therefore be the real test of whether this remains a contained AI/US growth correction or broadens into a wider global risk-off move.

Much depends on how we perform in the first few trading sessions next week, but my view is that this is a reset rather than a bubble bursting.

Broadcom did not report disastrous numbers, nor did it disprove the AI infrastructure story. The problem was expectations. Investors wanted another NVIDIA-style confirmation that AI demand was accelerating even faster than already aggressive assumptions. Instead, Broadcom delivered guidance that was good, but not good enough for a market priced for perfection.

That distinction is crucial for investors to understand. The AI thesis has not broken, but the market is starting to demand more discipline. The past few months have seen a near-parabolic move in parts of the semiconductor complex. In that environment, fundamentals can remain strong even as share prices correct. That is not contradictory; it is what happens when investors move from underestimating a theme to extrapolating it in too straight a line.

The strong US jobs numbers added another layer of pressure. Non-farm payrolls rose by 172,000 in May, comfortably ahead of expectations of around 85,000, while the unemployment rate held at 4.3%. March and April were also revised higher by a combined 93,000, which made the report harder to dismiss as a one-month anomaly. Job gains were led by leisure and hospitality, local government and healthcare, suggesting the labour market remains broader and more resilient than investors had assumed.

For the economy, that is good news. For markets hoping for near-term Fed relief, it is less helpful. Rate futures moved quickly after the data, with the probability of a Fed hike by December rising sharply, while the two-year Treasury yield rose to around 4.15% and the 10-year to around 4.5%. The problem for expensive growth stocks is not that the economy is collapsing; it is that it may be too firm for the Fed to cut while oil remains elevated and inflation risks persist. The AI trade can live with strong earnings, but it is more vulnerable when those earnings are paired with higher-for-longer rates, rising yields and no obvious help from the central bank. The weakness in Bitcoin added to the sense that speculative liquidity was being withdrawn from the higher-beta end of markets, rather than this being a simple earnings disappointment in semiconductors.

In addition, the job numbers underline that this does not look like a recession scare. It feels more like a valuation and discount-rate adjustment. The US economy still appears robust, corporate earnings remain resilient, and the consumer has not cracked. The issue is that the most crowded parts of the market had started to price in a very smooth path. For a more sustainable bull market to continue, I am happy with periods when the ‘froth’ is blown off markets. The long-term drivers remain intact: hyperscaler capex, data-centre demand, memory, networking, power, cooling, cybersecurity and automation. TSMC’s warning that chip supply will struggle to keep up with AI-fuelled demand for years actually supports the medium-term thesis. The issue is not whether AI is real. It clearly is. The issue is whether some share prices had begun to discount too much good news too quickly.

Indeed, a broader rotation would not necessarily be a bad thing either. One of the risks in recent weeks has been that leadership has become too concentrated among AI winners. If capital moves out of the most crowded semiconductor names and into a wider range of equities, that could help extend the bull market. If, however, weakness spreads into credit, defensives and broader earnings expectations, the message would be more concerning. At this stage, it is probably just a warning shot rather than a regime change.

Plainly, the Middle East remains the other major risk. The hoped-for clean peace deal has not arrived. US and Iranian forces exchanged fresh attacks overnight on Friday, with US Central Command reporting that it intercepted missiles and drones in the Persian Gulf and responded with strikes on Iranian radar sites. Missiles aimed at Bahrain and Kuwait were intercepted, drones heading towards the Strait of Hormuz were shot down, and fighting between Israel and Hezbollah continued. This was the worst flare-up since the ceasefire began and highlights how fragile the situation remains.

Diplomacy has not collapsed, but progress is slow. Trump still wants a deal, not least because high fuel prices are politically dangerous ahead of the US midterms. The broad outline remains an extension of the truce, with steps towards reopening the Strait of Hormuz and further talks on Iran’s nuclear programme. But the sticking points are substantial: frozen Iranian assets, nuclear concessions, shipping guarantees and a parallel ceasefire between Israel and Lebanon. Oil reflects that uncertainty. Prices are not at panic levels, but they remain materially above pre-war levels, with WTI above $90 and Brent near $93. That is high enough to keep inflation pressure alive through fuel, transport, food and producer costs. The market has moved from acute Hormuz panic to duration risk. That is less dramatic day-to-day but still economically important.

Back at home, the UK remains caught between slowing growth and sticky inflation. The composite PMI fell to 49.7 in May from 52.6 in April, pointing to little or no growth in Q2. Services slipped into contraction, while construction was very weak. April GDP is probably heading lower, partly reversing March’s gain and reflecting strikes and softer activity. There may be some offsets. Recent data suggest the consumer credit remained resilient, mortgage approvals rose, and car registrations recovered from April’s sharp fall. Household and business inflation expectations also eased, giving the Bank of England some comfort that second-round effects are not spiralling. However, wage and price signals remain sticky. Firms still expect elevated unit-cost growth, output-price expectations remain uncomfortable, and wage growth appears to have plateaued rather than continued to fall.

That leaves the Bank of England boxed in. Growth is softening, but inflation is not yet benign enough for the MPC to declare victory. A rate hike this year is now a close call rather than a certainty, but the Bank has little room to turn dovish quickly. The UK equity market continues to behave more defensively than the domestic economy, helped by the FTSE 100’s international earnings base, value bias and sector mix.

Europe faces a similar problem, but with even greater energy sensitivity. If oil falls and Hormuz gradually reopens, Europe benefits quickly. If the risk premium persists, Europe remains the most obvious developed-market casualty. The region’s equity markets have held up reasonably well, but the macro mix remains fragile: weak demand, imported energy pressure and limited room for central banks to look through inflation.

Asia is more finely balanced. China and Japan were relatively firm on the week, but they had not fully digested Friday’s late US sell-off. The region remains highly exposed to the AI supply chain, particularly through Taiwan, Korea and Japan, so that a deeper semiconductor correction would matter. But Asia is also the physical manufacturing layer of the AI cycle: foundries, memory, equipment, power components and advanced industrial supply chains. A US semi correction does not invalidate that structural role, but it may test near-term positioning.

So where does this leave us? Still broadly constructive, but acknowledging that this is a big test for the shorter term market narrative. The bull case is still that AI earnings remain strong, US growth stays resilient, the Fed avoids overtightening, and a messy but workable Iran deal eventually brings oil lower. In that scenario, last week’s sell-off will look like a healthy correction in an overextended theme. The bear case is that the AI correction becomes self-reinforcing, bond yields rise further after strong labour data, oil remains elevated, and investors begin to question whether earnings can continue to absorb higher discount rates.

That is not our base case, but it is a risk we are prepared for.

For now, this does not look like the bubble bursting. It looks like the market forcing discipline back into the most crowded part of the rally. Broadcom did not kill the AI trade; it showed that the bar had become too high. A period of consolidation would be healthy if it allows leadership to broaden. But the next few sessions really do matter. If Asia and Europe absorb Friday’s US weakness calmly, the correction can remain contained. If selling broadens, investors may start to question whether this is more than a reset.

This Week…

Next week’s first test will be market behaviour itself. Do investors buy the dip in AI infrastructure, or does the sell-off continue into Asia and Europe after Friday’s late US weakness?

US inflation data and Fed commentary will also matter after the strong jobs report. Sticky inflation would reinforce the higher-for-longer message and keep pressure on expensive growth stocks. A softer inflation print would ease some of that pressure.

Geopolitics remains the wild card. A credible US-Iran ceasefire extension and a path towards reopening Hormuz would be supportive. Further attacks around the Gulf would quickly bring oil and inflation risk back to the front of the market’s mind.

Tom McGrath 07.06.2026

Edited by Ash Weston 07.06.2026

DOWNLOADS

There are currently no downloads associated with this article.